There are several terms that a majority of respondents report understanding such as contribution, enroll and rollover.

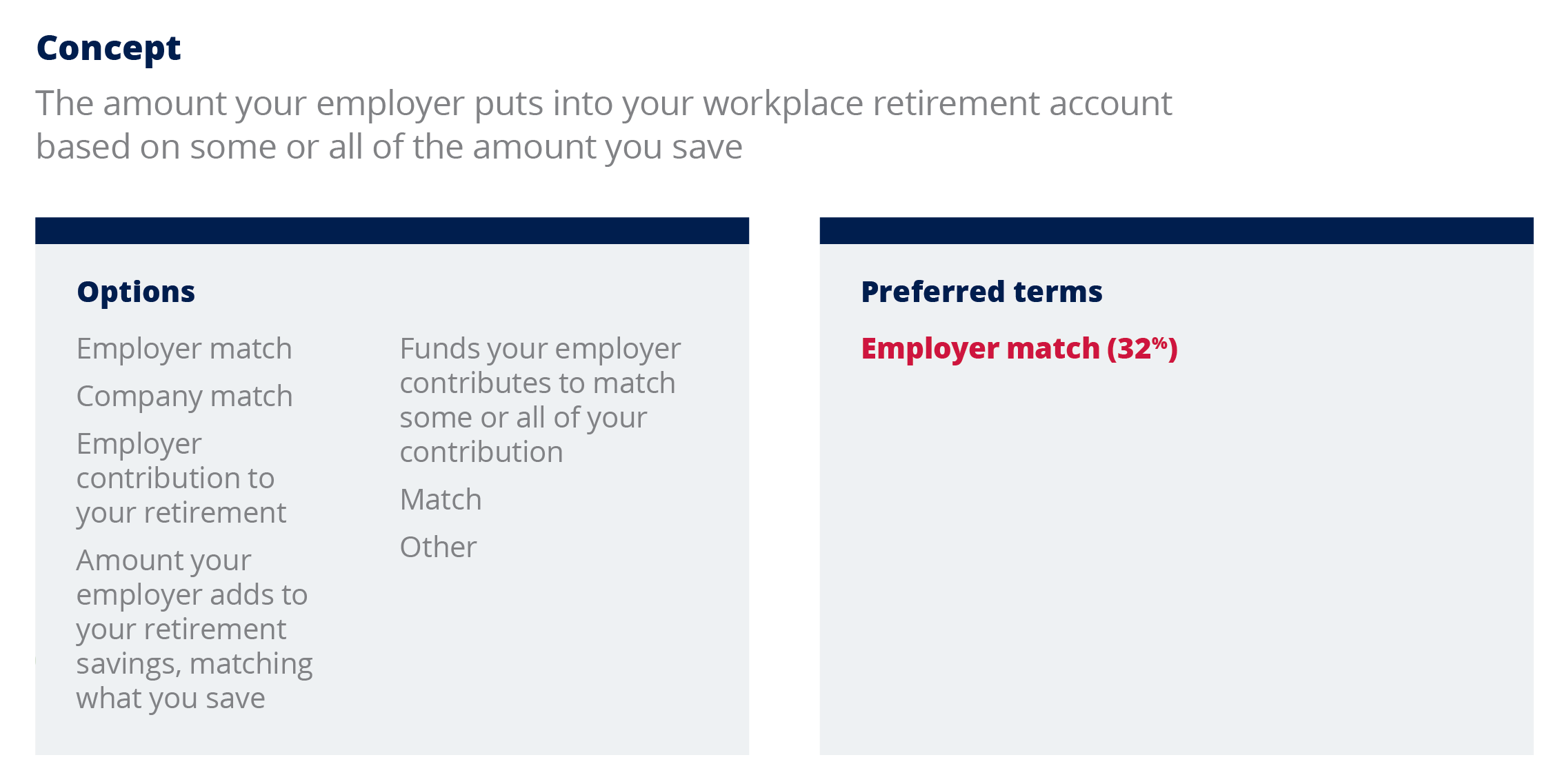

With small tweaks, jargon can be understood. An example is to use the term employer match instead of match.

Never miss a story — sign up for PLANSPONSOR newsletters to keep up on the latest retirement plan benefits news.

Personal email is preferred over all other means of communicating.

Words have the potential to inform, encourage and empower. But the wrong words can be powerful in negative ways, leaving people uncomfortable, overwhelmed or confused. Using the right words is especially critical in financial matters. Employees need to understand their retirement plan options so they can make the best decisions for their future, but the general public often misunderstands words that are commonly used by financial providers, employers and others in the retirement planning industry.

In fact, original Empower Retirement research has found that many terms frequently used in the industry simply don’t make sense to savers. However, the research also revealed some good news: Even small tweaks can help break down complex ideas and make important financial information accessible to plan participants. Employers can support their participants by making their retirement communications easy to understand and free from jargon, then delivering them via the method of communication employees prefer.

Below we explain why commonly used language in financial information is difficult for many readers to digest and offer research-backed tips on boosting clarity.

Think back to the last time you watched a court proceeding on TV or went to the doctor’s office. You probably heard some words whose definitions you didn’t know with certainty or maybe at all. Those words may have sounded highly technical — something you’d refer to as jargon.

Every profession has its own set of jargon. For professionals working within a particular field, that trade-specific lingo is a sort of shorthand that gets the point across quickly to colleagues who share that language. But to an outsider, the language can be alienating. (See A jargon grab bag below.) Jargon is particularly troublesome because industry insiders often don’t recognize when they’re using it.

Now consider some of the words typically used in workplace retirement plan communications, such as contribution or match. These terms are readily understood by employers, service providers, consultants and the business media. But how do employees view these words?

Consider the following examples of plan terms that have different meanings in common use: 1

Amount expected of an item in short supply

When it comes to retirement planning, all of these terms have meanings that are completely out of step with the definitions most people associate with them. Such multiple meanings can cause confusion and create barriers to confident decision-making.

For employees choosing savings strategies for retirement and trying to make sure they’ll have enough to live on, the stakes are high. It’s important for financial providers and employers to know what employees understand and how best to communicate with them.

We conducted three studies spanning 12 months to find out what individuals understand, and what they don’t, when it comes to financial and retirement-industry jargon. (See below.) We also asked about preferences for retirement plan communications. Our goal was to find out how to communicate more effectively with plan participants.

Overall, we found many commonly used industry terms don’t make sense to their intended audience. For example, 66% of respondents don’t understand what “rebalancing investments” means. A similar percentage — 69% — is unclear on the meaning of “asset allocation.” 2

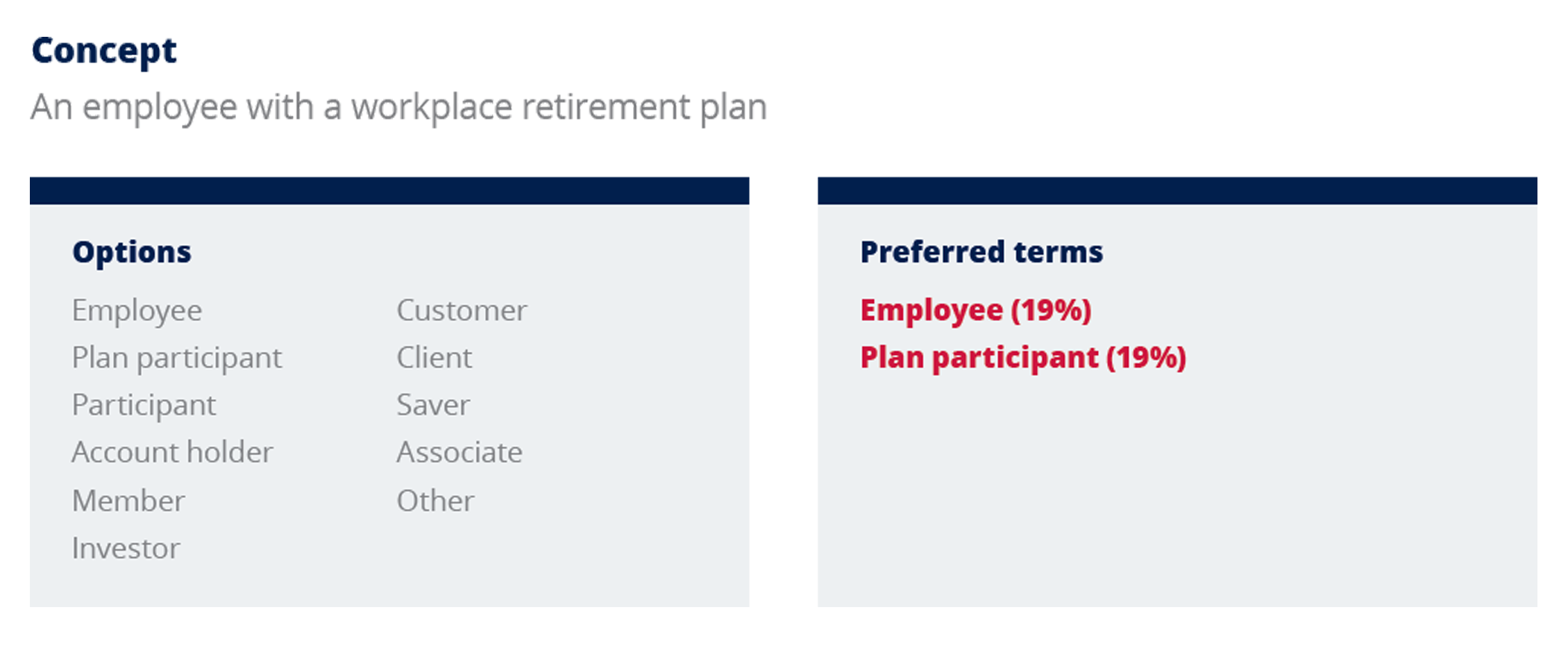

Millennials in particular found financial terms difficult to understand. This finding is consistent with academic research that shows younger age groups scored the lowest on both objective and subjective tests of financial literacy. 3 For example, 63% of millennial respondents found the term “plan participant” to be unclear compared with 44% of total respondents.

Given the lack of clarity across age groups, financial providers clearly have room to improve how they communicate about workplace retirement plans. 4 And it’s not just the vocabulary: Workers are also looking for higher quality retirement communications overall. Respondents consistently stated the following preferences:

As part of our efforts to understand which terms best convey the intended meaning, we showed respondents more than 20 common retirement planning concepts and asked them to select the most appropriate term for each concept from a list of terms. Ultimately, we found that terminology preferences vary. While there was no single term that was universally preferred for each concept, some general preferences did emerge.

Consider the following examples:

For a complete list of preferred terms, see the table at the end of this paper.

Though the survey revealed occasional differences in preferences based on age, in most cases, respondents’ preferences were consistent across age groups. Ultimately, we found terms that individuals across age groups understood. Based on these findings, we created a list of “safe words” — words and phrases we believe individuals would prefer to see in communications from their workplace retirement plans.

Effective communication considers not only how you say something, but where and when the message is received. If you deliver a message to a place where employees aren’t looking, the message won’t matter, no matter how well it’s constructed.

That’s why we asked survey respondents how they prefer to receive messages about their retirement plan. Personal email topped their responses both when we let them choose as many methods as they would like and when they had to select the most preferred method. One important finding: Only 26% of respondents said that work email is a preferred method for receiving plan communications, and even fewer chose it as their most preferred method.

Employees may prefer to get plan information via their personal email because that inbox is also home to their other financial communications, such as bank statements. Receiving plan information in the same place may make it easier for employees to think about their household finances, including retirement, in a holistic manner.

Financial matters are complex and confusing for many people. When the communications surrounding them are difficult to understand, topics only become more overwhelming.

Our research shows that many employees find common finance language lacks clarity. Consider whether the terms you’re using might be considered jargon to industry outsiders, and focus on simplifying language whenever possible.

Also make sure you’re reaching your audience where they are — whether that’s by email, on your website or somewhere else. In some cases, you may have to seek permission to communicate with employees via their personal email. Using the platform your readers prefer is a key step in helping them act on the information they need.

By providing clear information via the methods your employees prefer, you can help them be well-informed about their options and confident in their decisions.

1. Source: Jim Phillips, MarketWatch, “Decoding your 401(k) plan’s ridiculous jargon,” November 2013.

2. Source: Empower Retirement Employee Thought Leadership Research – June 2017, Market Strategies International, N=2000, 21+-yearold workers participating in their employers’ defined contribution plans.

3. Source: Xiao, J. J., Chen, C., & Sun, L., “Age differences in consumer financial capability,” International Journal of Consumer Studies, 39(4), 387-395, 2015.

4. Source: Empower Retirement Employee Thought Leadership Research – August 2018, Q8 Research LLC, N=1000, 21+-year-old workers participating in their employers’ defined contribution plans.

For General Informational Use Only – May Not Be Used for Guidance Purposes

The Empower Institute is brought to you by Empower Retirement and critically examines investment theories, retirement strategies and assumptions. It suggests theories and changes for achieving better outcomes for employers, institutions, financial advisors and individual investors.

Great-West Financial®, Empower Retirement and Great-West InvestmentsTM are the marketing names of Great-West Life & Annuity Insurance Company, Corporate Headquarters: Greenwood Village, CO; Great-West Life & Annuity Insurance Company of New York, Home Office: New

York, NY, and their subsidiaries and affiliates, including registered investment advisers Advised Assets Group, LLC and Great-West Capital Management, LLC.

IMPORTANT: The projections, or other information generated on the website by the investment analysis tool and Lifetime Income Score℠ regarding the likelihood of various investment outcomes, are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. The results may vary with each use and over time. Healthcare costs and projections, if applicable, are provided by HealthView Services. HealthView Services is not affiliated with GWFS Equities, Inc. Empower Retirement does not provide healthcare advice. A top peer is defined as an individual who is at the 90th percentile of the selected age band, salary range and gender.

Securities distributed through GWFS Equities, Inc., Member FINRA/SIPC and a subsidiary of Great-West Life & Annuity Insurance Company.

This material has been prepared for informational and educational purposes only and is not intended to provide investment, legal or tax advice.

Case studies are shown for illustrative purposes only and should not be relied upon as advice or interpreted as a recommendation. Results shown are not meant to be representative of actual investment results. Past performance is not a guarantee of, and may not be indicative of, future results.

The charts, graphs and screen prints in this presentation are for ILLUSTRATIVE PURPOSES ONLY.

Unless otherwise noted: Not a Deposit | Not FDIC Insured | Not Bank Guaranteed | Funds May Lose Value| Not Insured by Any Federal Government Agency

The trademarks, logos, service marks and design elements used are owned by GWL&A or used with permission.

©2019 Great-West Life & Annuity Insurance Company. All rights reserved. ERMKT-FBK-22524-1812 RO702882-0119